Qsbs Exclusion Chart

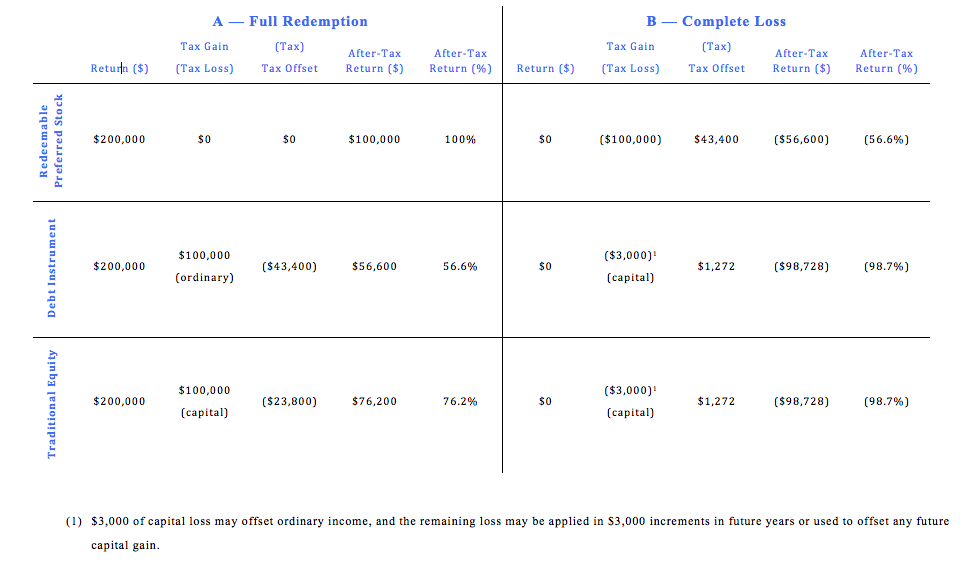

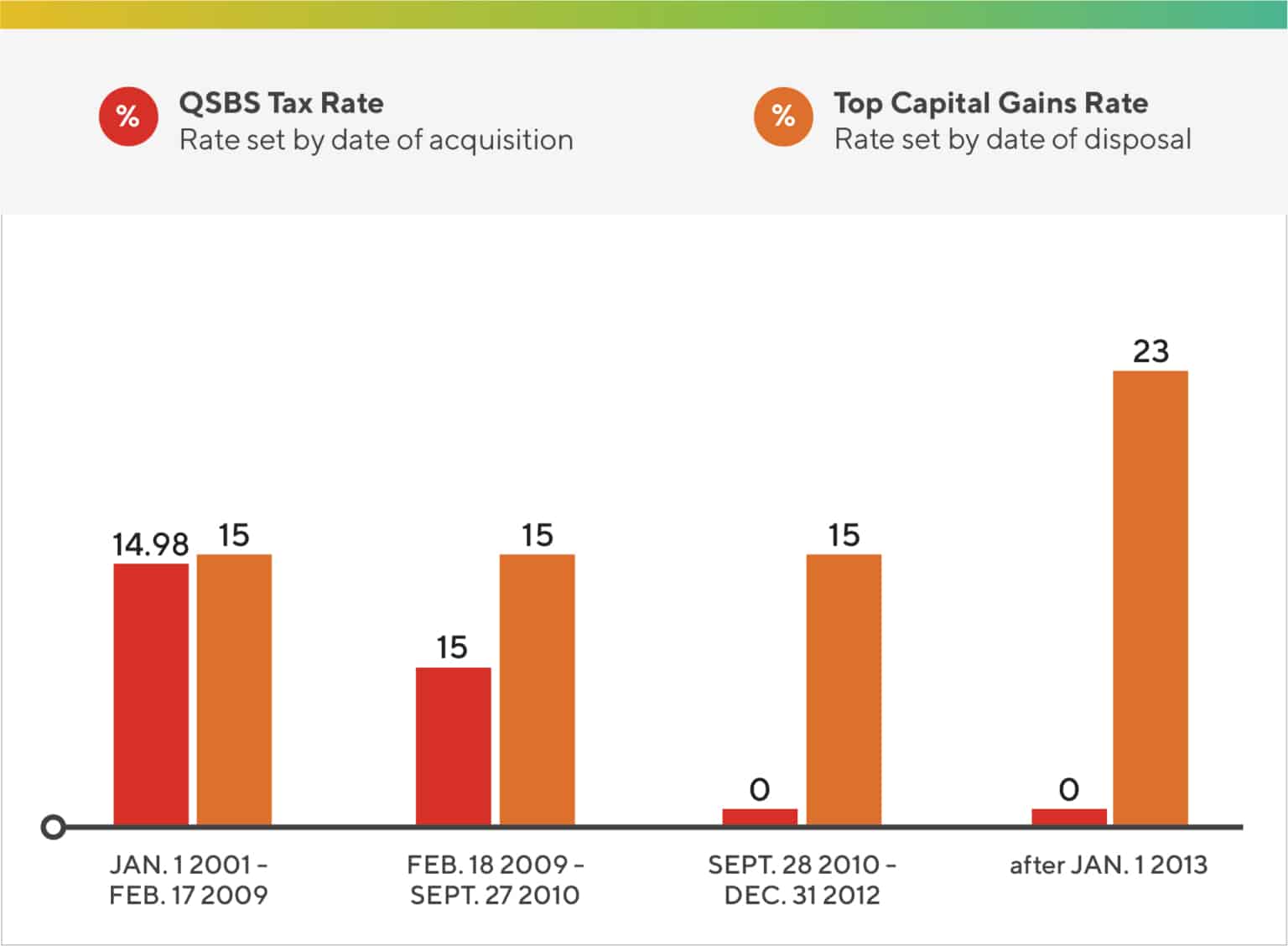

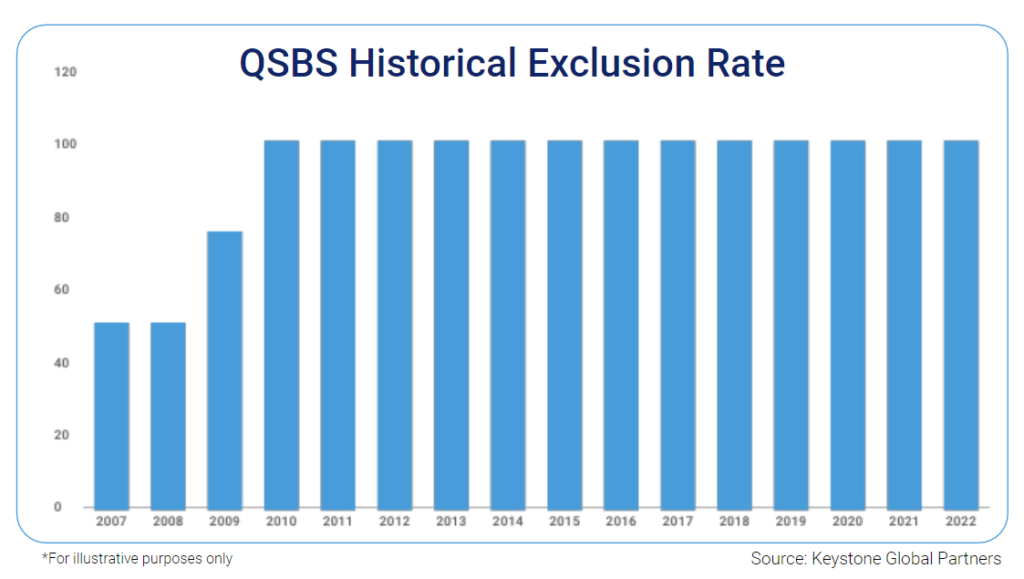

Qsbs Exclusion Chart - Web provided that you’ve held the qsbs (qualified small business stock) for at least five years you can exclude the greater of 10 times your initial investment or $10. Web initially, the exclusion was limited to 50% of the gain from the sale of qsbs held at least five years, but the capital gain was taxed at 28%, for an effective tax rate of. Web beginning in 2015, for the first time since its enactment in 1993, sec. Web for qualified small business stock (qsbs), there is an exclusion of gain limited to the greater of $10 million per taxpayer, reduced by prior eligible gains. When shareholders sell or exchange their qualified stock, the exclusion. Web generally, 50% of the gain can be excluded for qsbs issued after august 10, 1993, and before february 18, 2009; Web the qualified small business stock exclusion: Web qsbs enables taxpayers to exclude from their gross income all or a portion of the gain recognized from the sale or exchange of stock if certain conditions are met. 1202 was enacted to incentivize investment in certain small businesses by permitting gain exclusion upon the sale of qualified small business stock (qsbs). Web section 1202 allows stockholders to claim a minimum $10 million federal income tax gain exclusion in connection with their sale of qualified small business stock. Web the qualified small business stock exclusion: If the corporation underwent any significant redemptions, reorganizations or conversions, the tax treatment may be compromised. Web section 1202 is the tax provision that enables taxpayers to exclude capital gain on the sale of qualified small business stock (qsbs) if certain conditions are met. 1202 allows noncorporate taxpayers to exclude from federal income. Web qsbs enables taxpayers to exclude from their gross income all or a portion of the gain recognized from the sale or exchange of stock if certain conditions are met. When shareholders sell or exchange their qualified stock, the exclusion. Web as the charts illustrate, the exclusion of qsbs proceeds from capital gains tax is an attractive proposition. Web the. Web qsbs enables taxpayers to exclude from their gross income all or a portion of the gain recognized from the sale or exchange of stock if certain conditions are met. Web provided that you’ve held the qsbs (qualified small business stock) for at least five years you can exclude the greater of 10 times your initial investment or $10. However,. Web section 1202 is the tax provision that enables taxpayers to exclude capital gain on the sale of qualified small business stock (qsbs) if certain conditions are met. Web the qsbs regulations are located in internal revenue code (irc) section 1202 and include criteria for both the corporation to qualify as a qualified small business and criteria for. Web beginning. Web as the charts illustrate, the exclusion of qsbs proceeds from capital gains tax is an attractive proposition. Web the qsbs regulations are located in internal revenue code (irc) section 1202 and include criteria for both the corporation to qualify as a qualified small business and criteria for. Web provided that you’ve held the qsbs (qualified small business stock) for. Web generally, 50% of the gain can be excluded for qsbs issued after august 10, 1993, and before february 18, 2009; Web internal revenue code section 1202, also known as the qualified small business stock (qsbs) exclusion, provides a way to reduce those federal income tax liabilities by. Web the qualified small business stock exclusion: Web for qualified small business. Web qsbs enables taxpayers to exclude from their gross income all or a portion of the gain recognized from the sale or exchange of stock if certain conditions are met. Web section 1202 allows stockholders to claim a minimum $10 million federal income tax gain exclusion in connection with their sale of qualified small business stock. When shareholders sell or. Web the qualified small business stock exclusion: When shareholders sell or exchange their qualified stock, the exclusion. However, the rules of qsbs gain exclusion are complex and. Web qsbs enables taxpayers to exclude from their gross income all or a portion of the gain recognized from the sale or exchange of stock if certain conditions are met. Web section 1202. Web provided that you’ve held the qsbs (qualified small business stock) for at least five years you can exclude the greater of 10 times your initial investment or $10. When shareholders sell or exchange their qualified stock, the exclusion. Web initially, the exclusion was limited to 50% of the gain from the sale of qsbs held at least five years,. Web the qsbs tax exclusion is set forth in section 1202 of the u.s. Web the qualified small business stock exclusion: Web for qualified small business stock (qsbs), there is an exclusion of gain limited to the greater of $10 million per taxpayer, reduced by prior eligible gains. When shareholders sell or exchange their qualified stock, the exclusion. Web qsbs. Web qualified small business stock (qsbs) is stock that is eligible for the special tax rules created by section 1202 of the internal revenue code (irc). Web for qualified small business stock (qsbs), there is an exclusion of gain limited to the greater of $10 million per taxpayer, reduced by prior eligible gains. Web initially, the exclusion was limited to 50% of the gain from the sale of qsbs held at least five years, but the capital gain was taxed at 28%, for an effective tax rate of. Web internal revenue code section 1202, also known as the qualified small business stock (qsbs) exclusion, provides a way to reduce those federal income tax liabilities by. Web the qsbs tax exclusion is set forth in section 1202 of the u.s. Web the qualified small business stock (qsbs) gain exclusion under section 1202 can provide significant tax benefits by allowing an individual to exclude up to 100%. Web beginning in 2015, for the first time since its enactment in 1993, sec. Web as the charts illustrate, the exclusion of qsbs proceeds from capital gains tax is an attractive proposition. When shareholders sell or exchange their qualified stock, the exclusion. 1202 allows noncorporate taxpayers to exclude from federal income tax 100% of the gain on. Web generally, 50% of the gain can be excluded for qsbs issued after august 10, 1993, and before february 18, 2009; Web provided that you’ve held the qsbs (qualified small business stock) for at least five years you can exclude the greater of 10 times your initial investment or $10. Web section 1202 is the tax provision that enables taxpayers to exclude capital gain on the sale of qualified small business stock (qsbs) if certain conditions are met. 75% of the gain can be excluded for qsbs. If the corporation underwent any significant redemptions, reorganizations or conversions, the tax treatment may be compromised. 1202 was enacted to incentivize investment in certain small businesses by permitting gain exclusion upon the sale of qualified small business stock (qsbs).

Unlocking Growth and Tax Benefits A Comprehensive Guide to the QSBS

How the Section 1202 Exclusion Can Save Millions in Taxes Gordon Law

QSBS & SBS Chart Blue Dot Law

Section 1202 Stock The QSBS Gain Exclusion Founders Circle

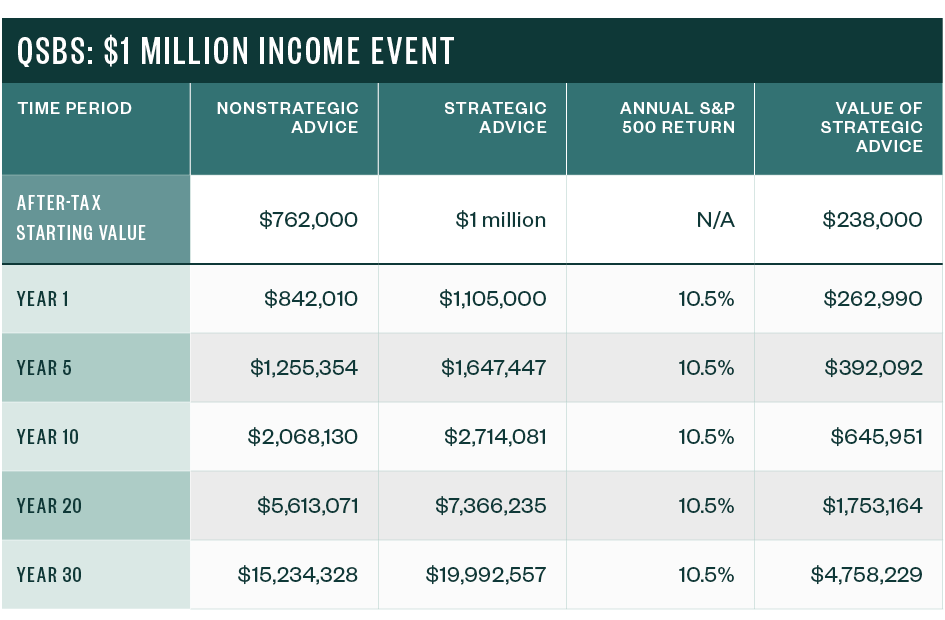

Compounded Value of Professional Advice for QSBS

Entrepreneurs’ Guide to Qualified Small Business Stock (QSBS

Founders’ and Entrepreneurs’ Guide to Qualified Small Business Stock

Top 3 Mistakes VCs Make with QSBS Aumni Blog

Qualified Small Business Stock (QSBS) Exclusion

How Much Tax Will You Owe When You Sell Your Company, And How to

Web Qsbs Enables Taxpayers To Exclude From Their Gross Income All Or A Portion Of The Gain Recognized From The Sale Or Exchange Of Stock If Certain Conditions Are Met.

Web Section 1202 Allows Stockholders To Claim A Minimum $10 Million Federal Income Tax Gain Exclusion In Connection With Their Sale Of Qualified Small Business Stock.

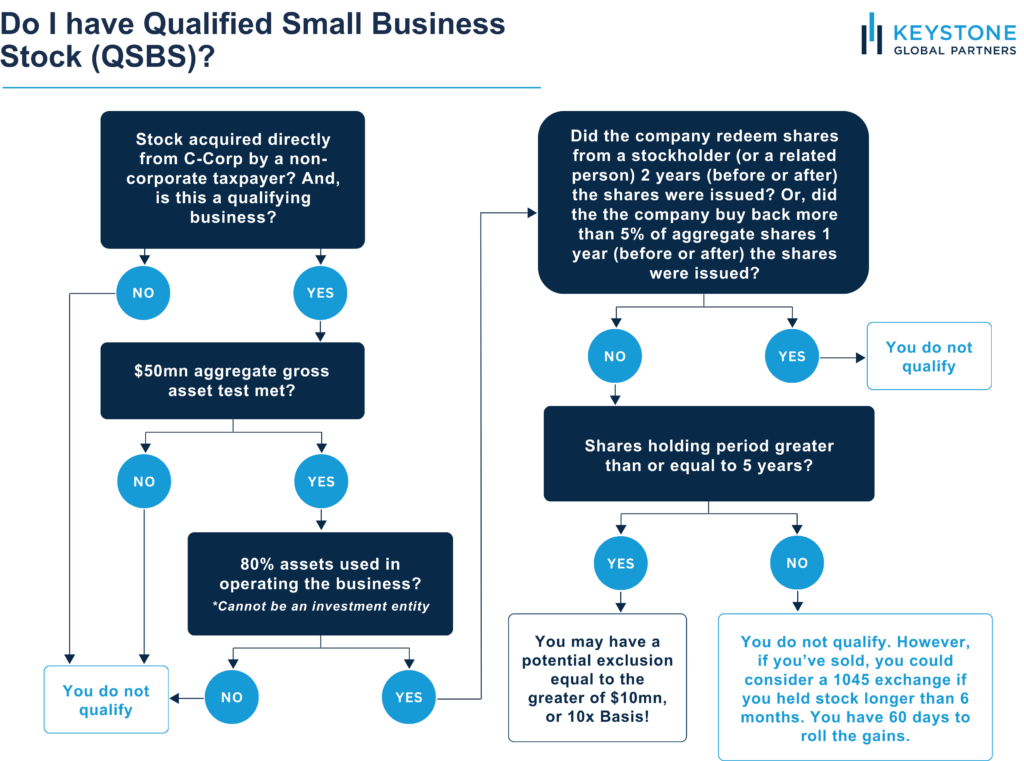

Web The Qsbs Regulations Are Located In Internal Revenue Code (Irc) Section 1202 And Include Criteria For Both The Corporation To Qualify As A Qualified Small Business And Criteria For.

However, The Rules Of Qsbs Gain Exclusion Are Complex And.

Related Post: