Clo Rating Chart

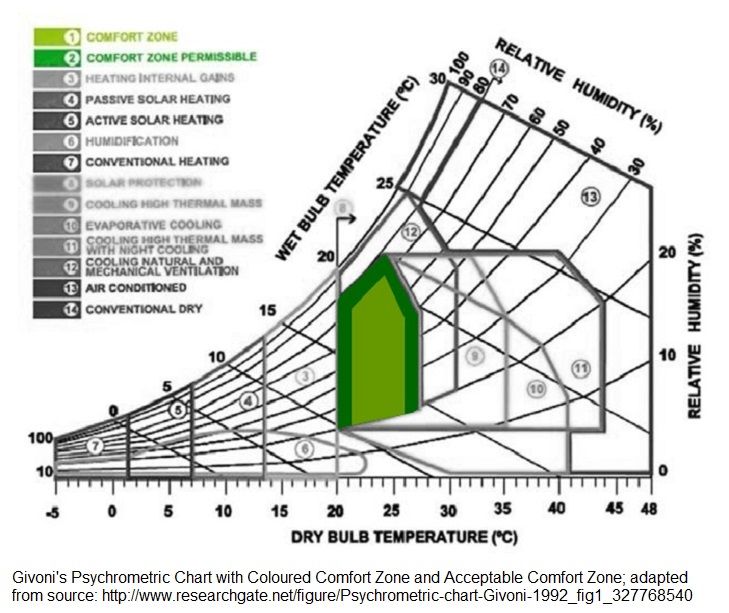

Clo Rating Chart - Web the averages in the chart reflect a mix of rating transition outcomes, including ratings that do not experience any change, ratings that move a single notch and ratings that move more than one notch. This can relate each default scenario to the asset and liability side cashflow. Synthetic insulators provide more insulation per. Web from 2010 through 2023, s&p global ratings rated 14,204 classes from more than 1,750 u.s. The important thing here is that unlike fill power, clo is not a characteristic that is unique to one ounce of the material. Rating clos and cdos of large corporate credit. Web the clo is related to the comfort zone in the psychrometric chart because it is assumed people wear clothing while in buildings; Clos and corporate cdos rating criteria. Clo 2.0 transactions totaling over $1.07 trillion (including refinancing and reset activity). Clo asset classes will be rated and monitored by dbrs morningstar using the following dbrs morningstar methodologies (collectively, the dbrs morningstar clo methodologies): These changes have no rating impact. Web the clo is related to the comfort zone in the psychrometric chart because it is assumed people wear clothing while in buildings; Fitch ratings has updated its global clo and corporate cdo rating criteria, replacing the existing version dated sept. This should be read together with the counterparty risk methodology. The update relates. The important thing here is that unlike fill power, clo is not a characteristic that is unique to one ounce of the material. Pants 1/2 long legs made of wool: The update relates primarily to the notching approach for issuer ratings on rating watch negative, which are notched by one sub category. Web clo value is the insulation power of. Only temperatures, relative humidities, and specific volumes which would allow people to continue wearing clothing are accepted as part of the comfort zone. 1 day −2.78% 1 week −0.68% 1 month −31.51% 6 months −73.94% year to date −74.02% 1 year −90.12% 5 years −93.93% all time −97.58% key stats. Synthetic insulators provide more insulation per. Web clo value is. Clo 2.0 transactions totaling over $1.07 trillion (including refinancing and reset activity). Web from 2010 through 2023, s&p global ratings rated 14,204 classes from more than 1,750 u.s. This can relate each default scenario to the asset and liability side cashflow. Except for assured/bluemountain sale, thrusting sound point to one of the top managers in active. No clos rated 'a'. For example, this value is 0.92 for 1 oz (28.35 grams) of a dry primaloft one for one square yard. Web as announced on july 23, 2020, any new transactions in u.s. Fitch ratings has updated its rating criteria for collateralised loan obligations (clos) and corporate collateralised debt obligations (cdos). Fitch ratings has updated its global clo and corporate cdo. The companies that issue the loans in mm clos, like other highly leveraged companies, have felt the impact of rising interest rates and. Fitch ratings has updated its rating criteria for collateralised loan obligations (clos) and corporate collateralised debt obligations (cdos). Pants 1/2 long legs made of wool: Fitch ratings has updated its global clo and corporate cdo rating criteria,. Only temperatures, relative humidities, and specific volumes which would allow people to continue wearing clothing are accepted as part of the comfort zone. I cl, clo m 2 k/w; Clo asset classes will be rated and monitored by dbrs morningstar using the following dbrs morningstar methodologies (collectively, the dbrs morningstar clo methodologies): No clos rated 'a' or higher were downgraded. Metaphorically, like fp * fw value in down jackets…and the higher the value is, the warmer the insulation is. Web the clo is related to the comfort zone in the psychrometric chart because it is assumed people wear clothing while in buildings; Web during 2020, s&p global ratings lowered just 1.3% of outstanding mm clo tranche ratings (seven out of. Web the averages in the chart reflect a mix of rating transition outcomes, including ratings that do not experience any change, ratings that move a single notch and ratings that move more than one notch. Web this methodology supplements our general structured finance rating methodology for the rating analysis of collateralised loan obligation (clo) transactions, and supersedes it in case. Web i a (clo) calm < 1 < 2 < 0.5 > 0.5; Pants 1/2 long legs made of wool: Web the clo is related to the comfort zone in the psychrometric chart because it is assumed people wear clothing while in buildings; The estimated loss is then distributed to each tranche using ejr proprietary modeling. Web clo value is. Fitch ratings is proposing updated assumptions in its global criteria for rating collateralized loan obligation (clo) notes. The companies that issue the loans in mm clos, like other highly leveraged companies, have felt the impact of rising interest rates and. Web the averages in the chart reflect a mix of rating transition outcomes, including ratings that do not experience any change, ratings that move a single notch and ratings that move more than one notch. Web the clo is related to the comfort zone in the psychrometric chart because it is assumed people wear clothing while in buildings; Web as announced on july 23, 2020, any new transactions in u.s. Clo asset classes will be rated and monitored by dbrs morningstar using the following dbrs morningstar methodologies (collectively, the dbrs morningstar clo methodologies): Pants 1/2 long legs made of wool: Web from 2010 through 2023, s&p global ratings rated 14,204 classes from more than 1,750 u.s. Web s&p global ratings emea collateral managers dashboard provides you with a snapshot view of your clo critical credit risk factors all in one place. Web fitch ratings reviews collateralized loan obligation (clo) documentation as part of its rating analysis. Clo value is an important factor in determining a synthetic jacket’s warmth. Only temperatures, relative humidities, and specific volumes which would allow people to continue wearing clothing are accepted as part of the comfort zone. Web this methodology supplements our general structured finance rating methodology for the rating analysis of collateralised loan obligation (clo) transactions, and supersedes it in case of conflict, inconsistency or ambiguity. No clos rated 'a' or higher were downgraded during the year. These changes have no rating impact. The estimated loss is then distributed to each tranche using ejr proprietary modeling.

(PDF) CLO Rating Methodology Scope Ratings DOKUMEN.TIPS

CLO Rating Chart In Powerpoint And Google Slides Cpb

![]()

Fitch Ratings WebBased CLO Tracker LSTA

An Introduction to Collateralized Loan Obligations (2022)

The Lead Left CLOs Revisited Ratings, Risks, and Returns (Last of a

CLOs

Global Association of Risk Professionals GARP

PPT Structured Finance Synthetic ABS PowerPoint Presentation, free

FAQ

The Clo and Thermal Comfort THE environmental ARCHINEER

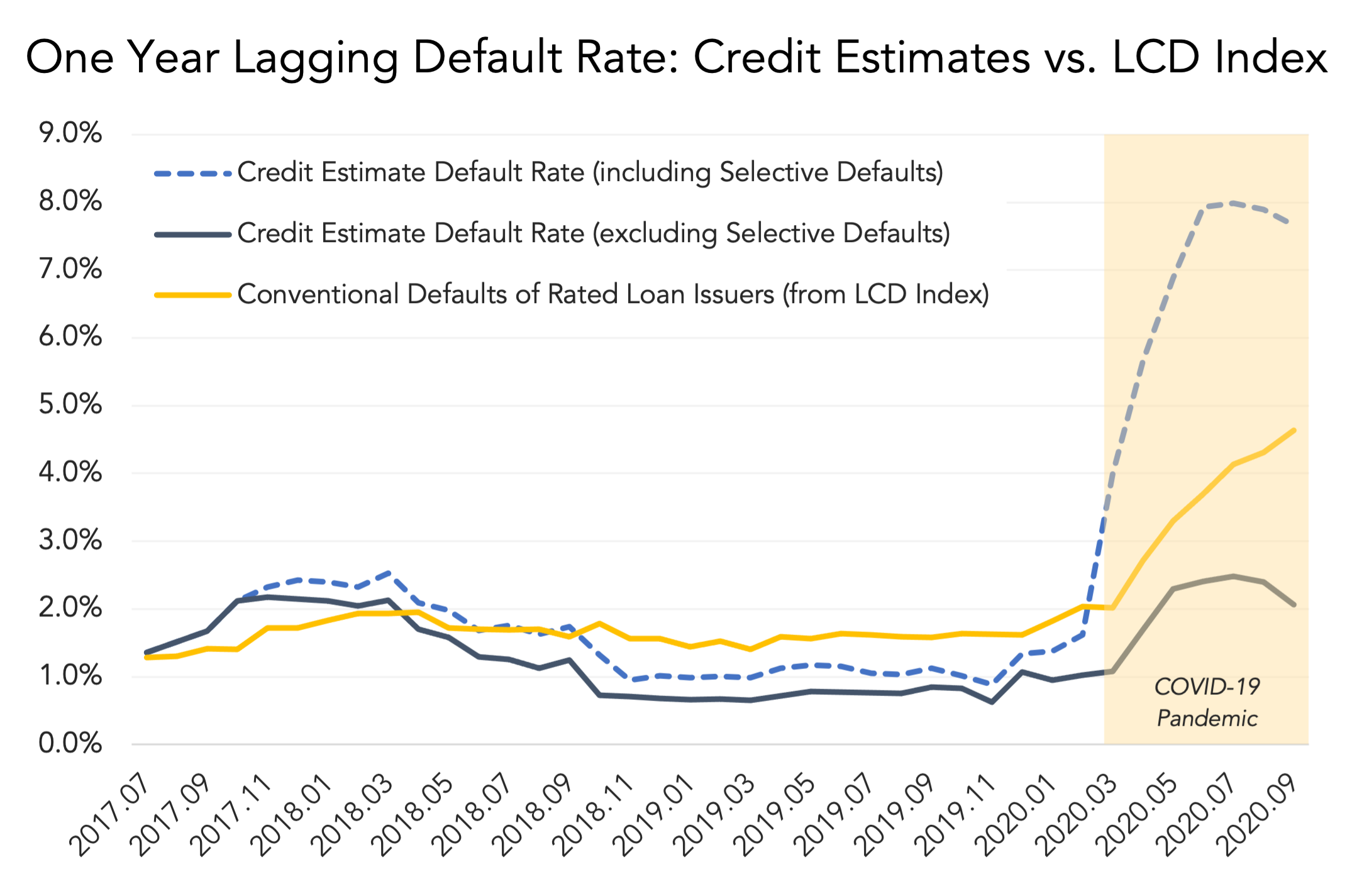

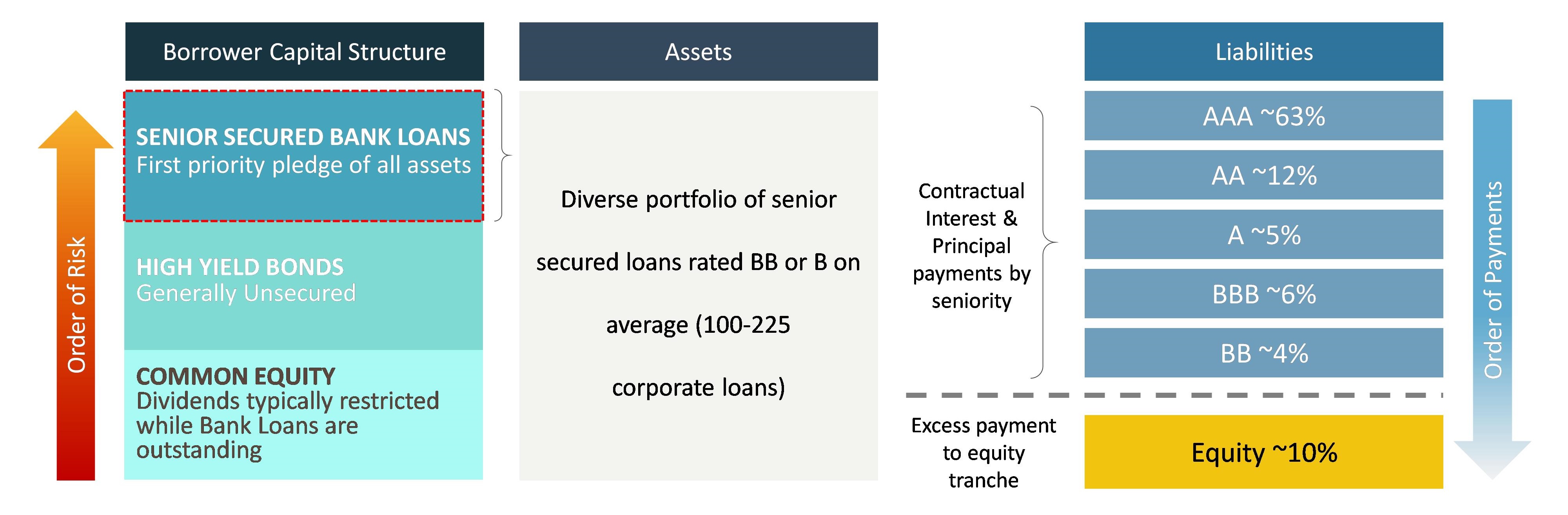

Web Ejr Ratings Of Clo Tranches Are Based On The Estimated Losses (El) Generated By Applying Historical Default Scenarios Based On Likelihood Of Occurrence.

Web During 2020, S&P Global Ratings Lowered Just 1.3% Of Outstanding Mm Clo Tranche Ratings (Seven Out Of 553 Outstanding At The Time), Compared To About 13% (493 Out Of 3,786) For Bsl Clo Ratings.

Web Our Clo Rating Methodology Captures Shifting Risk Conditions In The Loan Market Through Its Use Of Recovery Ratings ('1+' Through '6'), And These Are Currently Available For More Than 95% Of The Assets Found In U.s.

Our Interactive Tool Provides Clarity To Examine, Compare And Benchmark Individual Emea S&P Global Ratings Rated Clos Across A Series Of Key Performance Indicators To Help You.

Related Post: