163 J State Conformity Chart

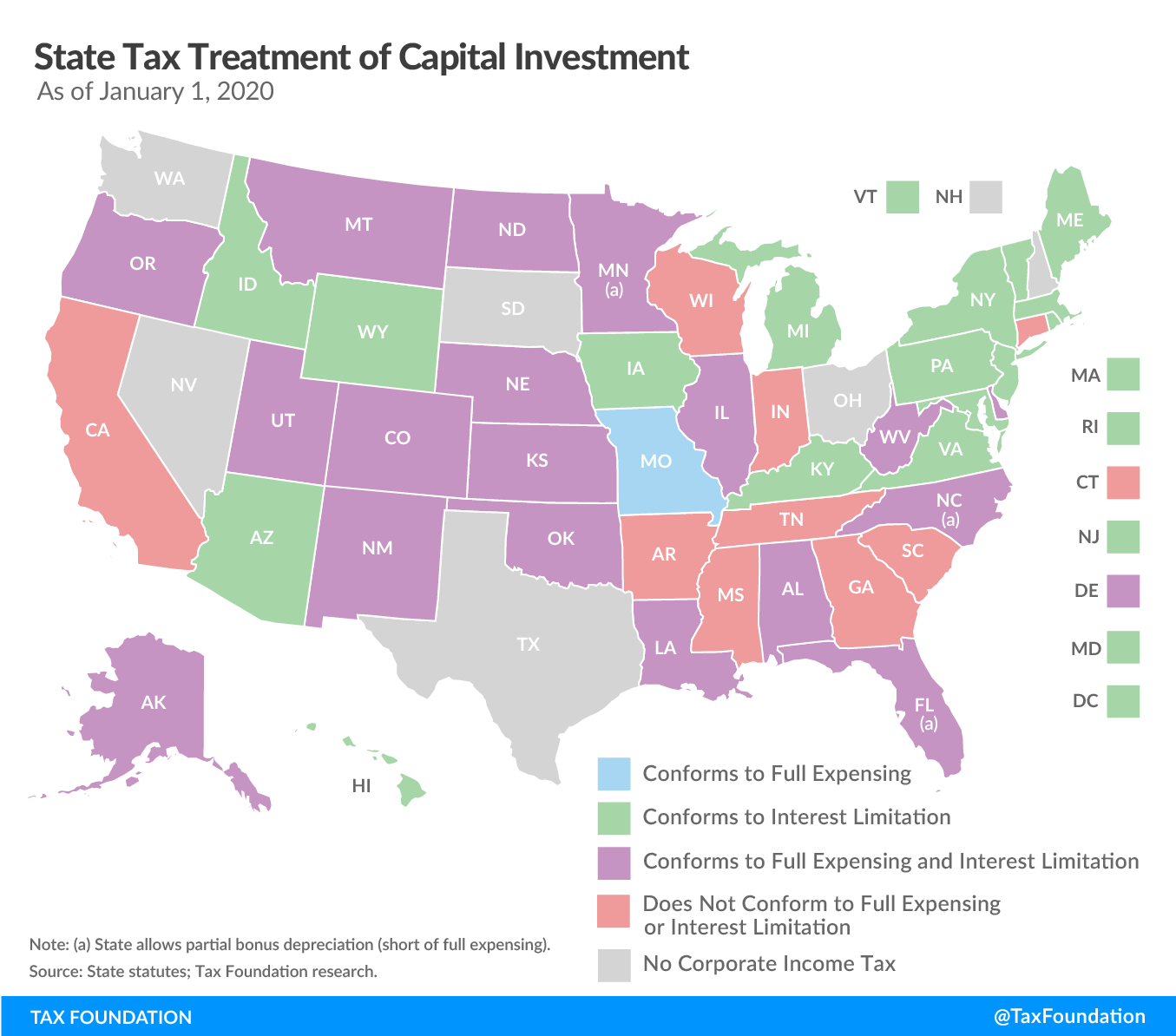

163 J State Conformity Chart - Conformity chart, which includes each state’s conformity status, key differences between state and federal bonus depreciation rules, state resources, and expert analysis to help simplify your corporate tax planning strategy and reduce risk. 163 (j) carryforwards to the definition of prechange losses (sec. 381 and 382, so it is important not only for federal purposes, but also for state purposes, to accurately calculate and track the sec. Web most states, absent legislative decoupling, generally will conform to section 163 (j), but how they conform will depend upon subtle differences in how each state conforms to that section of the irc and its regulations. 163 (j) business interest expense deduction limitation; Web the tcja amended sec. Web this study aims to highlight the importance of a systematic approach to process capability assessment and the importance of following a sequence of steps. Web under section 163 (j), a taxpayer's business interest deduction cannot exceed the sum of: Web state conformity to the code: Web companies also should consider state conformity to, and treatment of, section 280c, the potential for state subtraction modification for disallowed federal deductions, and the impact to a taxpayer’s section 163 (j) limitation. Web the tcja amended sec. 163 (j) business interest expense deduction limitation; Web state conformity with section 163(j) is complicated. Web this paper provides a snapshot of how states currently conform to internal revenue code (irc) income tax provisions in general, as well as to the irc’s treatment of nols, business interest expenses, forgiven ppp loans, and uc benefits. Conformity. Most states have adopted secs. Some states, such as new york, have already decoupled from the cares act section 163(j) provision (retaining the 30% limit). Web state conformity with section 163(j) is complicated. Web calculation of limitation for state corporate income tax purposes. Web as for conformity to the internal revenue code, approximately 35 states currently adopt section 163 (j). Some states, such as new york, have already decoupled from the cares act section 163(j) provision (retaining the 30% limit). • the taxpayer's floor plan financing interest for. Business interest expense limitation under § 163 (j) paycheck protection program income exclusion and expense deduction. This study evaluates the process capability of crown cap manufacturing through. Net operating loss (nol) deduction. That conformity, however, is far from uniform. Most of the 22 states with “rolling” business and corporate tax conformity will automatically adopt the cares act tax provisions. Web a comprehensive federal, state & international tax resource that you can trust to provide you with answers to your most important tax questions. The chart below provides a basic irc conformity overview.. 163 (j) limitation resulting from the consolidated group's aggregate amount of bie, bii, and ati, computed without regard. Most of the 22 states with “rolling” business and corporate tax conformity will automatically adopt the cares act tax provisions. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense. 163 (j) business interest expense deduction limitation; 381 and 382, so it is important not only for federal purposes, but also for state purposes, to accurately calculate and track the sec. Web companies also should consider state conformity to, and treatment of, section 280c, the potential for state subtraction modification for disallowed federal deductions, and the impact to a taxpayer’s. Web companies also should consider state conformity to, and treatment of, section 280c, the potential for state subtraction modification for disallowed federal deductions, and the impact to a taxpayer’s section 163 (j) limitation. Most states have adopted secs. Conformity chart, which includes each state’s conformity status, key differences between state and federal bonus depreciation rules, state resources, and expert analysis. Specifically, the new regulations did not provide further guidance on the section 163(j) treatment of: Web state conformity with section 163(j) is complicated. Web april 1, 202124 min read by: Web chart 1 illustrates the status of state corporate income tax law conformity with the federal interest expense deduction limitation after the cares act.10 eleven states did not adopt or. Web tcja/cares act conformity maps. One of the most significant tax changes for many businesses in 2022 is a requirement that taxpayers capitalize and amortize their research and experimentation (r&e) expenses paid or incurred after dec. 381 and 382, so it is important not only for federal purposes, but also for state purposes, to accurately calculate and track the sec.. 163 (j) business interest expense deduction limitation; 381 and 382, so it is important not only for federal purposes, but also for state purposes, to accurately calculate and track the sec. This study evaluates the process capability of crown cap manufacturing through. Web download the full state i.r.c. And (4) net operating losses (nols). Most of the 22 states with “rolling” business and corporate tax conformity will automatically adopt the cares act tax provisions. Roughly 23 states and the district of columbia have rolling conformity to the internal revenue code for corporate income taxes, where the state's definition of taxable income is automatically updated to the currently enacted code. 163 (j) make clear that a federal consolidated group has a single sec. Most states have adopted secs. Web under section 163 (j), a taxpayer's business interest deduction cannot exceed the sum of: 163 (j) carryforwards to the definition of prechange losses (sec. Web download the full state i.r.c. One of the most significant tax changes for many businesses in 2022 is a requirement that taxpayers capitalize and amortize their research and experimentation (r&e) expenses paid or incurred after dec. Web the proposed regulations under sec. 163 (j) limitation resulting from the consolidated group's aggregate amount of bie, bii, and ati, computed without regard. Business interest expense limitation under § 163 (j) paycheck protection program income exclusion and expense deduction. Conformity to the irc and associated amendments. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules, and qualified improvement property asset life, and nol carryback in the cares act and tcja. Web this study aims to highlight the importance of a systematic approach to process capability assessment and the importance of following a sequence of steps. Web as for conformity to the internal revenue code, approximately 35 states currently adopt section 163 (j) for purposes of their corporate income taxes. Some states, such as new york, have already decoupled from the cares act section 163(j) provision (retaining the 30% limit).

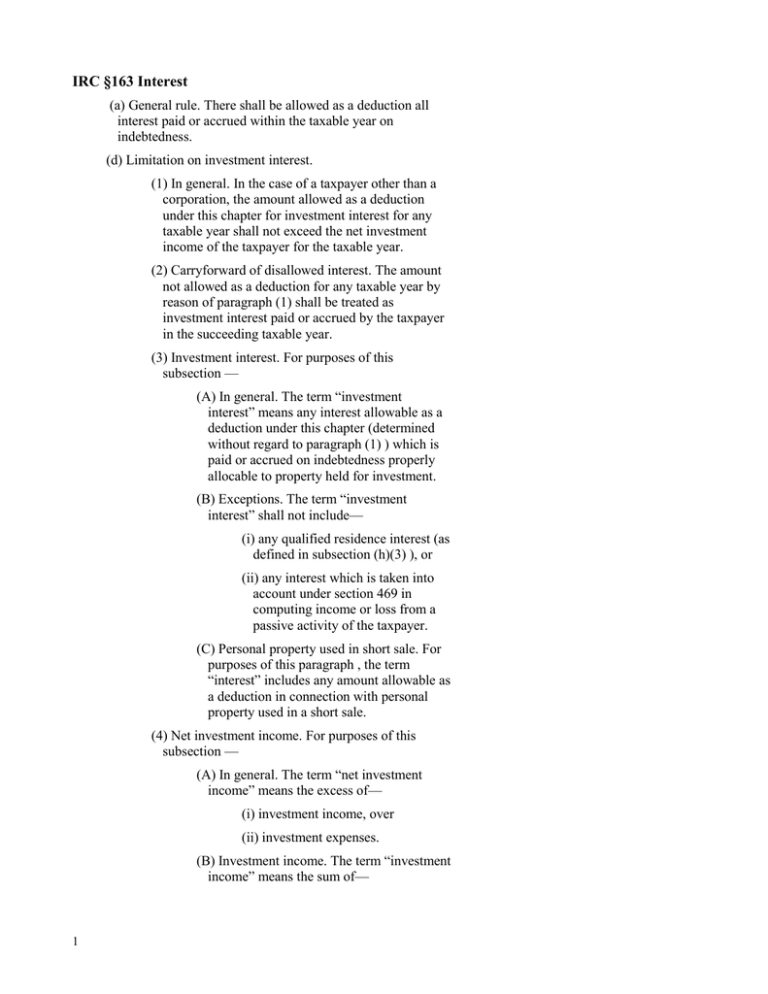

IRC §163 Interest

The State of Federal Conformity Tax Foundation of Hawaii

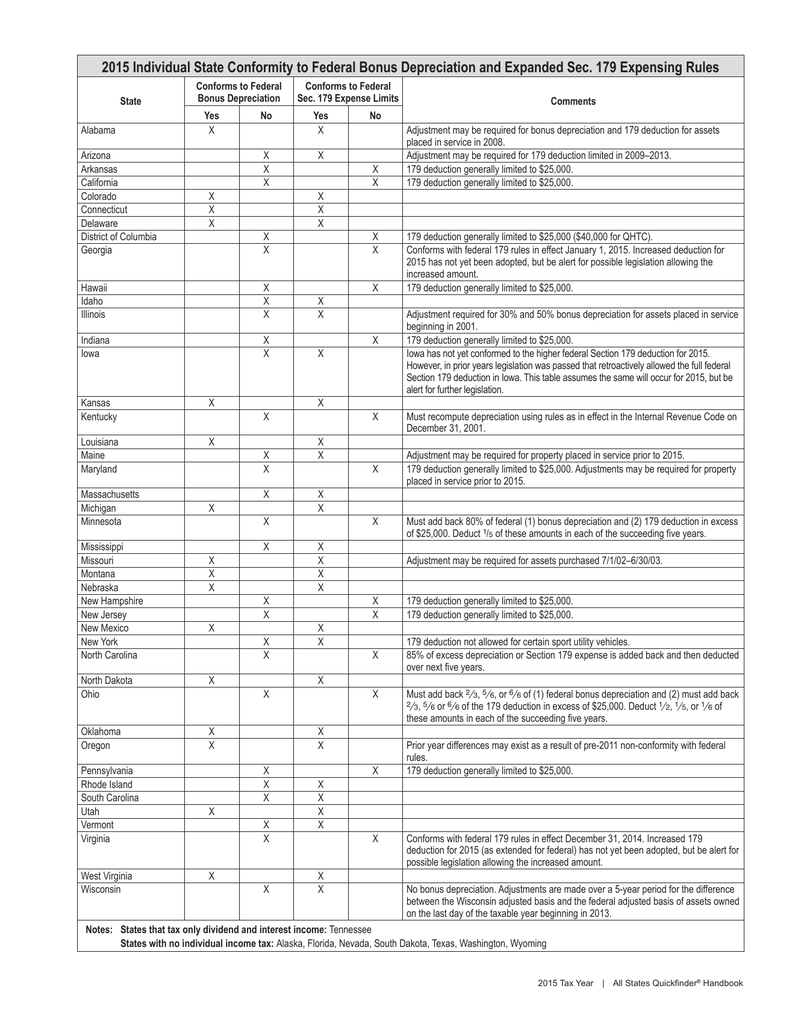

2015 Individual State Conformity to Federal Bonus Depreciation and

State Tax Conformity a Year After Federal Tax Reform

State Conformity to CARES Act, American Rescue Plan Tax Foundation

State Conformity to CARES Act, American Rescue Plan Tax Foundation

State Conformity to Federal PandemicRelated Tax Provisions in CARES

Will Arizona Lead the Way on Full Expensing This Year? Upstate Tax

TCJA Proposed Regulations Weekly Client Update 163(j) Interest

State Tax Conformity a Year After Federal Tax Reform

Currently, A Majority Of States Conform To Irc Section 163 (J).

• The Taxpayer's Floor Plan Financing Interest For.

Specifically, The New Regulations Did Not Provide Further Guidance On The Section 163(J) Treatment Of:

That Conformity, However, Is Far From Uniform.

Related Post: